Do your loan applications get rejected due to the presence of inaccurate information in your CIBIL report? You are not alone, nowadays, it has become one of the common problems among the borrowers. In this scenario, it’s very crucial to ensure that the information mentioned in your CIBIL report is accurate, complete and up-to-date. Otherwise, it will not only hamper your CIBIL score but also damage the possibility of further loan approval. In this article, we have discussed the common errors that you can find in a CIBIL report, and the complete process to rectify CIBIL report.

What is CIBIL report and what factors affect a CIBIL score?

In simple terms, a CIBIL report is a summary of a borrower’s credit history and loan repayment records that’s used by creditors to evaluate and approve loan applications. Typically, TransUnion CIBIL gathers credit information from various lending institutions, including PSU Banks and NBFCs. Based on the repayment records, they generate a numerical score for each individual borrower, known as the CIBIL score.

The CIBIL score is a 3-digit numeric representation, ranging from 300-900. A CIBIL score of 750 and above is considered as good, indicating responsible credit behaviour and creditworthiness of a borrower. Additionally, a CIBIL score works as a first impression for the lenders, having a high CIBIL score also helps you to secure a loan quickly with lower interest rates and more favourable terms and conditions.

Typically, the CIBIL score is calculated based on four main aspects: payment history, credit utilisation, credit mix between secured and unsecured loans, and new credit inquiries.

Now, what if someone else’s loan account is added to your credit report? What if you notice an overdue or outstanding balance in your already closed loan account or find mistakes in your loan repayment history? Additionally, you may find incorrect personal information, duplicate accounts, and unauthorised loan inquiries in your CIBIL report. These are common errors that you might encounter in your CIBIL report.

In CIBIL’s own words, issues in an individual credit report can be categorised into major two parts:

- Inaccurate information reflected on a borrower’s credit report; which mainly occurs due to the mistake by lenders or some technical issues in TransUnion CIBIL or due to the miscommunication between them.

- Default of the loan repayment; occurs when the borrower fails to repay their debt.

Any kind of error mentioned in your CIBIL report can cause a severe drop in credit score and lead to financial stress.

Common types of error in a CIBIL report:

Data Mixing error:

In recent times, data mixing error is one of the most common mistakes in a CIBIL report. Because of that, you can notice unrecognizable loan accounts, incorrect personal information and credit inquiries mentioned in your CIBIL report, which may lead to a severe negative impact on your credit score.

Especially, when your KYC details such as your Name, DOB, Residential Address, and identification details are very similar to another person’s; then a data mixing error happens. Consequently, someone else’s loan accounts can be reported in your CIBIL report.

Not only loan accounts, but you may also find unknown addresses, contact details, and unauthorised credit enquiries included in your CIBIL report.

If you are facing the same kind of issue, then you should rectify errors in CIBIL report immediately; otherwise, it will hamper your creditworthiness.

Inaccurate outstanding balance and loan status:

You have paid off your debt and closed the loan account, but the loan account still shows as ACTIVE on your CIBIL report. According to the banking system, every lending institute updates their consumer data to TransUnion CIBIL once a month.

Therefore, when you clear your dues, it will take an average of 30-45 days to reflect in your CIBIL report. However, if more than two months have passed and the loan status has not been updated yet, then it is an issue. Mostly, this type of error arises due to the negligence of the lenders.

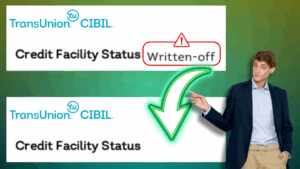

As we discussed earlier, the CIBIL score is significantly influenced by the customer’s repayment history. Therefore, any inaccurate outstanding balance, overdue amounts, or default statuses such as Written-off, Suit filed, Settled, etc. can severely impact your credit score. It would be best if you corrected the loan status urgently by raising a dispute in CIBIL.

Incorrect delay payments in repayment history:

In some special cases, it’s also seen that a borrower is paying his loan EMI’s timely, but the lender reports incorrect delayed payments on the borrower’s CIBIL report.

In general, DPDs or Days Past Due denote the number of days by which the borrower has delayed his loan EMIs. It should be ‘STD’ or ‘000’, otherwise it will be viewed negatively by the lender. In fact, the terms ‘SMA (Special Mention Account)’, ‘DBT (Doubtful)’, and ‘LSS (Loss)’ may create a severe drop in CIBIL score. So, check your loan repayment history thoroughly, and rectify all the delayed payments if it is not genuine.

Duplicate loan accounts:

In some cases, you may notice your same loans/ credit card account reported twice in your CIBIL report. This will increase the total number of active accounts in your CIBIL report, which can impact negatively and reduce your CIBIL score remarkably.

This kind of error arises due to a technical fault and can be removed easily by raising an online dispute in CIBIL.

Incorrect credit limit assignment:

Sometimes, you may notice incorrect credit limit is reported in your CIBIL report. For example, earlier your credit card limit was 30K. Recently, the lender increased your credit card limit by 50K but they forgot to update the same to your credit report.

Now, this may affect your credit utilization ratio and consequently impact negatively on your CIBIL score. That’s why, check your credit card limits that are mentioned in your CIBIL report and rectify them if it’s not updated properly.

Default loan account due to non-payment:

Now, if you genuinely default your loan EMIs or haven’t paid your credit card bill for a long period, then your loan account will be reported as delinquent in your CIBIL report. This is not exactly an error; this happens due to the fault of the borrower.

Any kind of default status like overdue, Written-off, Suit filed, Wilful default or settled remark will hit your CIBIL score negatively. Even, lenders will find it risky to approve any further credit facility.

So, if you missed some of your loan’s EMIs because of job loss or unforeseen circumstances, then it’s best to repay the due immediately and rectify errors in CIBIL report to get back your CIBIL report on track.

The process to rectify CIBIL report and improve CIBIL score:

Now, to remove all the inaccurate information from your CIBIL report, you have to raise your concern to TransUnion CIBIL and the respective lender, who have reported the wrong information in your CIBIL report. Here, we have discussed the complete process, so that you can rectify your CIBIL report smoothly by following a few steps.

Step 1: Check your CIBIL report and identify the error:

If your CIBIL score is poor and your loan application is rejected repeatedly, your first step should be to check your CIBIL report and identify any specific errors. To do this, visit TransUnion CIBIL’s official website (www.cibil.com) and obtain your annual free report.

Next, thoroughly read your CIBIL report, which is divided into five main sections: Personal Information, Contact Information, Employment Information, Account Information, and Enquiry Information. The most crucial section is Account Information. Examine each loan account carefully, including its repayment history to identify any specific errors.

Step 2: Raise a dispute in CIBIL:

After identifying the error, you need to raise a dispute in TransUnion CIBIL. There are mainly two ways to raise disputes in CIBIL.

I. Raise an online dispute by logging into my CIBIL Portal:

To raise an online dispute with CIBIL, log in to your my CIBIL portal using your CIBIL user ID and password. Navigate to the ‘Raise a dispute’ section. Update the incorrect information with the correct details and then submit the dispute. After successful submission, a Dispute ID will be generated, so save it for future reference.

II. Write a complaint letter in CIBIL:

In the previous methods, there was no option to attach any documents that support your claim. That’s why, it is not enough to rectify errors in CIBIL.

Therefore, you need to write a complaint letter in CIBIL, where you have the opportunity to describe your problem along with the evidence, such as KYCs, payment receipts, No Dues Certificate, etc. Ensure to mention the CIBIL control number in the complaint letter. Upon completing the process, you will receive a Service Request Number.

Step 3: Send an email to the CIBIL Nodal:

In general, CIBIL takes approximately 30 working days to resolve your dispute. Now, in case, they fail to resolve your dispute or you are not satisfied with their response, then you can send an email to the CIBIL Nodal Officer at nodalofficer@transunion.com or the CIBIL Escalation Desk at escalationdesk@transunion.com after 30 days from the initial dispute date. Don’t forget to mention your previous Dispute ID and Service Request Number in the complaint letter to receive priority attention.

Step 4: Send a request to the lender:

As per RBI provisions, TransUnion CIBIL has no authority to make changes to your credit report without getting confirmation from the lender who reported the incorrect information. Therefore, you can file a separate complaint with the lender for a quicker resolution.

In addition to this, you can reach CIBIL through different channels, like their Customer Care Number (022 – 6140 4300), CIBIL Chatbot, and send a letter to their registered office address: TransUnion CIBIL Limited, One World Centre, Tower 2A, 19th Floor, Senapati Bapat Marg, Elphinstone Road, Mumbai – 400013.

This is the all-about rectification process, Hope this will help you to rectify errors in CIBIL report and improve your CIBIL score.

Read more:

- How to remove “Suit Filed” from CIBIL report?

- How to remove “Fraud Loan” from CIBIL report?

- How to remove “Settled” status from CIBIL report?

Pingback: Why did Experian credit score drop suddenly?

Pingback: How to contact CIBIL customer care?

Pingback: How to write complaint in CIBIL through Emails?

Pingback: How to get Business Loan with Low CIBIL Score?