Table of Contents

In today’s digital payment era, credit cards offer great convenience for online purchases, like extra discounts on bills, attractive rewards, cashback, and much more. However, it also comes with the responsibility of repaying the used amount timely. Any missed or delayed payment can put you in a debt trap and severely damage your credit score. So, whether you are a new credit card user or someone managing multiple cards, it is very important to understand how does credit card late payment affect CIBIL score.

In this blog, we will cover the impact of credit card late payments, their consequences on your credit score, and share some pro tips on using credit cards wisely to maintain a healthy credit profile.

What is Credit Card late payment in CIBIL?

Generally, when you avail a credit facility, whether it’s a loan or a credit card, the respective lender issues a due date by which you have to repay the money borrowed. Missed or delayed payment beyond this date is recorded in your CIBIL report and termed as late payments.

Especially for a credit card, when you make a purchase on your credit card, your card issuer typically pays to the merchant on your behalf. At the end of the billing cycle, your card issuer sends you a total bill that you’ve spent on your credit card throughout the month. There is a specific date by which you’ve to make the payment.

At that point, you have two options: Either pay the full outstanding amount to avoid interest charges, or pay only the minimum due amount (usually 5–10% of the outstanding balance). However, if you fail to make even the minimum payment before the due date, it is considered a delayed payment. Such delays are reported as DPD (Days Past Due) in your CIBIL report.

Now, let’s understand how does credit card late payment affect CIBIL score.

How does Credit Card late payment affect CIBIL Score?

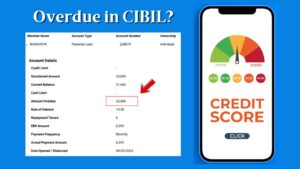

Do you know, almost 35% of your total credit score solely depends on repayment history? That’s why, when you miss or delay your credit card bill, a single delayed payment causes a severe impact on your CIBIL score; it may cause an average 20-50 points dip in your credit score. Now, if you default for consecutive months, the delay status increases progressively to 30, 60, 90, 120 days, and so on, causing even greater damage to your credit score.

Apart from these, when you default on your credit card payments, lenders impose penalty charges as per their internal policies. These pending due (Minimum payable amount + penal charges)are reported as “Overdue” in your credit report, further affecting your score negatively.

Continuing to default on credit card bills may lead you into a heavy debt trap and cause of severe negative consequences in your CIBIL report, such as Written-off, Suit Filed, and Willful Default. Such remarks can permanently damage your creditworthiness and make you ineligible for future loans or credit approvals.

How do you manage credit card debt to maintain a healthy credit score?

Now, you’ve understood well, how does credit card late payment affect CIBIL score and damage your creditworthiness. If your credit score has already been affected by credit card payments, then you have to be financially disciplined to rebuild your credit score. Follow a few effective tips to manage your credit card debt and maintain a healthy credit score.

➤ Pay your credit card bill timely:

After every billing cycle, make sure to pay at least the minimum due amount to avoid any negative impact on your CIBIL score. To ensure timely payments, you can set up an auto-debit option or align your billing cycle right after your salary credit date. This will help you manage payments smoothly and on time.

➤ Keep your credit utilisation low:

To maintain a healthy credit score, it is important to keep your credit utilisation low—ideally below 30% of your total credit limit. This helps keep your credit card debt manageable and shows that you are not overly dependent on credit. As a result, it has a positive impact on your overall credit score.

➤ Pay more than the minimum due amount:

There is a very common question: Does paying minimum due on credit card affect CIBIL score? Technically, not, if you continue to pay at least the credit card minimum due, it is not considered a late payment, and does not have any negative impact on your credit score. However, paying only the minimum due for several months can push you into an unmanageable debt trap.

For example, let’s say on May 1, you make a purchase of ₹10,000 on a credit card with an interest rate of 3% per month. Instead of paying the full amount, you choose to pay only the minimum due (5% of the outstanding balance) at the end of each month, without making any new purchases.

By the time you clear your balance at the end of six months (December), you will have paid around ₹15,600 — that’s 56% more than your original spend.

Even worse, if you continue paying just the minimum amount, your repayment period could stretch to nearly 9 years!

That’s why, if you have sufficient funds, it’s always better to pay more than the minimum due. Doing so helps you manage your credit card debt more effectively and avoid unnecessary interest.

This is all about the topic: how does credit card late payment affect CIBIL score. I hope you found it useful. If you have any questions or would like to share your opinion, feel free to comment—I’ll be happy to help.”